I’m at home today, the third and final day of an emergency trip home to visit my dad who’s not had the best of health this 2017. I’ve been grateful that I could come and visit at short notice and that all my siblings showed up this weekend to visit me. It’s the first time since November 2014 that we’ve all been in the same place and I feel nothing but love and gratitude for this opportunity. There’s a small downside, however! My flights here will take up 12 hours by the time I get back to London and I’d have only spent about 24 quality hours with my dad before I leave. It’s only because I’m currently beholden to work and could not, in good conscience, abandon my colleagues for longer than this whilst we were in the middle of the most important phase of our delivery cycle. So, this morning I woke up and just had to make another attempt at a FIRE PLAN.

Hopefully there will be many more days like this one even as I plan for FIRE

My previous FIRE plans, which I should probably point out are super vague and hopeful, are:

- Draft 1: Liberty within 12 years: I expected to have paid off all my debt and maxed out my emergency fund (EF) with 6 months of expenses by the end of 2017, save circa £18,000, use geographical arbitrage to keep my spending at £12,000 a year before 68 and use the state pension to keep annual spending from my portfolio post 68 at around £3,500. Woah!

- Draft 2: Liberty within 12 years: I expected to have paid off all debt and maxed out my EF by the end of 2018, save £24,000 a year, spend £12,000 (from the portfolio) per year post retirement and raise that to £20,000 post 55.Interest rate assumed to be 4% on average. That seemed more realistic.

How is my current plan any different?

A maths-based FIRE plan

What do I know about this year?

- My savings rate is currently around 53%

- I’ll have my baby emergency fund of £1,000, nearly £3,000 in cash savings, £1,200 in bonds and around £6,000 in my pension by the end of 2017

- I should have £12,000 of debt left to pay by the end of 2017

What assumptions have I made about my savings rates & plans for 2018 – 2028?

- Interest rates will average around 4% over time

- My salary will grow by around £12,000

- I will be predominantly employed, with a company matched pension, for the entire time except for 2023 when I will take a year off work

- My spending – including giving and support – will stay around £18,000 a year post 2018

- I retire early on 13th October 2028 having hit my magic number

How am I going to FIRE?

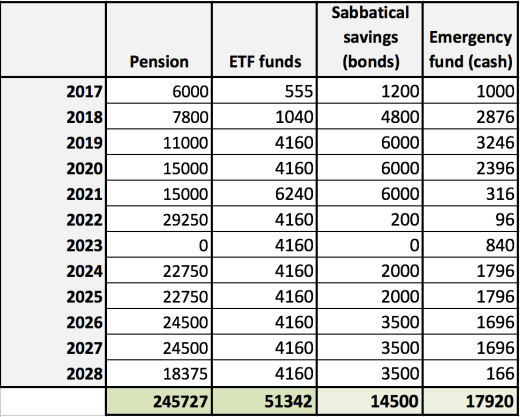

My summary of how much I need to save, where and how.

Notes

- My emergency fund will cover more than 1 year’s spending and will only be used for emergencies. Replenishing this fund will be part of my annual spending.

- My savings rate varies from 43% to 58% for the 12 years except the year I’m on a sabbatical when I shall be moving savings as opposed to saving anything new.

- My sabbatical savings will be held in the same NSandI bonds that I’ve currently got them in so will be stable but not necessarily interest earning. I will take out the £23,000 saved up by 2023 to fund my ETF funds and the mini-retirement that I will take that year. The remainder of the funds will be cashed out for spending in the first year of retirement.

- The first 5 years post retirement, I’ll either live a nomadic (thus cheap) lifestyle OR be doing a PhD that includes a stipend and thus will be able to spend an average of £15,000 per year for 20 years.

- £200,000 of my pension pot will remain intact for 20 years at least to fund my traditional retirement post 65. This should grow to £444,516 which is more than enough to fund my expected annual spend

- I plan to spend around £20,000 a year from 2068 – possibly supplemented by a state pension of £8,000 a year for a max yearly expense of £28,000. The £8,000 excess could cover healthcare or giving if I don’t need it for my regular spending.

- Because I would have travelled the length and breadth of the world from 45-64, I won’t have much travel planned and will thus be content with the occasional trip and a largely crafty, gardening, knitting or other such hobby-centric life post 65.

- I expect to continue to live in European countries where healthcare is either free or costs around £80 a month for private insurance.

What do you think? Is this overly ambitious? I’ve kept interest rates lower than I expect. Quitting being employed and contracting (something that could be a reality post 2019) could make the timeline shorter but since there are way too many unknowns, I have kept this plan fairly conservative.

from someone who has experienced a family members ill health and tied to work, do what you can to spend more time with your family member. Work will always be there and your coworkers can handle covering you.

LikeLike

Thank you. Yes, certainly. If I’d discovered he wasn’t any better then I’d have stayed longer but (fingers crossed), this way I’ve assuaged my fears and will be able to relax with the family for 2/3 weeks around Christmas too.

LikeLiked by 1 person