My financial knowledge was eerily shoddy in the past

I just found some tracking that I attempted to do in 2015 when I first realised that I was on a sinking ship and the cupfuls of water I was bailing out would no longer suffice. Here’s how bleak my life used to be 2 and a half years ago

Started from the (scary) bottom…

09.03.15

A summary of my situation as I captured it on this date

- Earning: £2244

- Spending: At least £2800 per month while adding more people to my list of creditors

- Key expenditure:

-

- £585 (Rent)

- £165 (Bills – housing)

- £216 (Public transport)

- £500 (Debt)

- £250 (travel)

- £400 (Socialising)

- £200 (Food/toiletries)

I moved out of London cutting my 3-4 hour daily commute to a half hour and with the hope that I would cut back on socialising.

05.06.15

Three months after that, I captured my situation again.

- Earning: £2285

- Spending: At least £2900 per month while paying off my creditors

- Key expenditure:

-

- £400 (Rent)

- £0 (Bills – housing)

- £130 (Public transport)

- £342 (Debt)

- £516 (travel)

- £328 (Socialising)

- £215 (Food/toiletries)

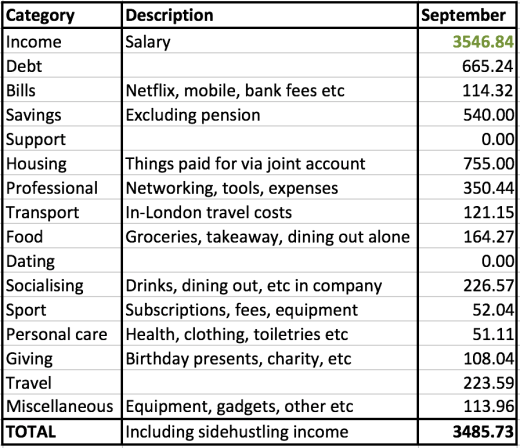

I was earning more money but haemorrhaging more. You can imagine how much borrowing, fear and worry living in this state engendered. I had no savings and as you can see from what I was tracking, I didn’t even know how to track properly. I didn’t pay attention to the details. I thought the broad picture would suffice. What do things look like now?

I’m not perfect at tracking – I need to change how I track money that I lend to people and when it’s refunded as I think that’s caused some of that difference between earnings and spending. You can see there are some savings, debt is being paid off and most importantly, I’m living within my means.

Achievements in the last year

I might not be where I need to be or moving at the pace I want to but I am moving and things are improving. Here’s a few things that I’ve done since last August when I started moving in the right direction:

- I’ve earnt over £6,000 in side-hustle income

- I’ve supported my family or given money to friends or charitable causes to the tune of nearly £8,500

- I’ve increased my pension from £0 to over £5, 000

- I’ve got a baby emergency fund of £1,000

- I’ve got £3,000 in other savings

- I’ve paid for trips to Berlin, Budapest, Vienna, Paris, Edinburgh, and Albufeira in cash

- I’ve paid off around £8, 000 of debt

- I haven’t borrowed any additional money

I still have my 2017 goals to hit – I’m still closer to the spendthrift end of the spectrum – and, with less than 3 months left of the year to achieve them, it’s easy to feel shitty.

However, I look at that list and it’s not too shabby. So, when I spend more than I want to or grab a round of drinks at the bar even though I know that costs more than paying for only my drinks, I’ll know that I needn’t worry (too much) because I’ve got some stuff figured out now. I just need to put more systems in place so that I can figure out all the others.